ARE BIG PROPERTY VALUE INCREASES GOING TO MEAN BIG TAX INCREASES?

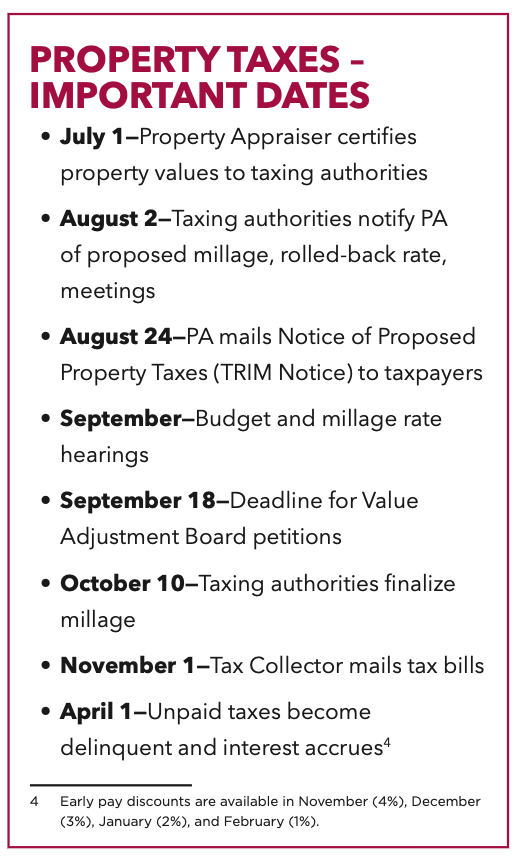

Florida’s housing market is raging, with growth in property values not seen since the housing bubble. Property appraisers certified the state’s taxable value for 2022 on July 1 and these values are currently being used by local governments and school districts in setting new property tax rates and developing budgets for FY 2022-23. The growth in property values has set the stage for what could be significant tax increases for Florida’s citizens and businesses.

The value of existing homestead property appreciated by 28.0 percent in 2022, even higher than the 2006 peak of 26.0 percent. While the housing market has historically been the driving factor in Florida’s total property value growth, in 2022 high growth was the case for all property classes. All property types appreciated by 25.0 percent in 2022, including big increases in the value of vacant and agricultural lands.

There was also significant new construction, which added another 2.2 percent growth to total property values.

Exemptions (such as the homestead exemptions) and assessment caps (such as Save Our Homes) reduce the just (fair market) value of the property for tax purposes. After these are deducted, the result is taxable value. School taxable value is the amount to which school districts’ millage rates are applied. On average, school taxes make up just under 40 percent of Floridians’ almost $40 billion total property tax bill. Statewide school taxable value increased by 20.1 percent in 2022. This is more than triple the annual growth of the previous three years and the largest percentage increase since the height of the last housing boom (2006-07). All but four counties experienced double-digit growth and nearly a third (22) of Florida’s 67 counties had increases above 20 percent.

County taxable value is smaller than school taxable value due to more exemptions that apply. This is the taxable value used by all tax jurisdictions except for schools (counties, cities, and special districts). County taxable value grew by 14.6 percent in 2022. Statewide, county taxable value rose by $330.2 billion to reach $2.586 trillion. Applying current millage rates to this increase would result in $3.5 billion in additional property taxes.

The Revenue Estimating Conference met earlier this month to develop its new property tax forecast, which included the 2022 certified values discussed in this report. The state estimators do not expect the extraordinary growth in property values in 2022 to continue. The low interest rates that helped fuel this growth are (at least for now) becoming a thing of the past. This tightening of federal monetary policy will result in higher mortgage rates, dampening sales, and then price increases. While perhaps not spectacular, the new forecast predicts continued elevated growth in the short term. County taxable value is estimated to increase by 9.6 percent in 2023 and 8.7 percent in 2024, more than any other post-2006 year.

Big increases in taxable value mean big property tax increases, or at least the opportunity for local governments to raise taxes. If they keep the same millage rate, or even lower it slightly, significant tax increases are in store.

The state’s Truth in Millage (TRIM) law, provides the process for local government officials to adopt new property tax millage rates and mandates that the starting point is the rolled-back rate. This is the millage rate that would raise the same amount of property tax revenue in the jurisdiction as the previous year, when applied to the new tax roll (minus new construction). If the governing board proposes a millage rate that exceeds the rolled-back rate—even if the proposed rate in the same or lower than the current rate--it must advertise a Notice of Proposed Tax Increase.

Because of the huge growth in taxable value this year, many local governments looking to keep the same millage rate may find a unanimous vote is needed.

Florida TaxWatch has already seen local governments publicizing that they are not increasing their millage rate this year. But with the much higher values, keeping the millage flat still means a big increase in property tax bills.

Owners of homestead property that are in the same home as last year are shielded from much of these increases because of Save Our Homes (SOH), which limits the increase in the assessed value of homestead property to the lesser of 3.0 percent or inflation. But even they would see the biggest increase in their tax bill in a while, since high inflation translates into the maximum 3.0 percent cap for the first time since 2012. Further, not all owners of homestead property get the full SOH benefit, evidenced by the fact that even with the 3.0 percent cap, total homestead taxable value rose 13.4 percent.

As is usually the case, it is non-homestead property that bears the brunt of increasing property taxes. Since SOH does not limit property taxes, but instead limits assessed values on one segment of property taxpayers, it has resulted in a multi-billion tax shift. While non-homestead property has a 10 percent assessment cap, it is not as valuable as the SOH cap, and not just because the cap is higher. The non-homestead cap does not apply to school taxes (almost 40 percent of the average tax bill), does not allow portability, and the recapture provision makes it difficult to build up cap savings over time.

As local governments continue the process of adopting their property tax milage rates for FY 2022-23, Florida TaxWatch urges their elected officials to consider the impact of increasing property tax bills on Floridians and roll-back millage rates as far as is prudent. This is especially true of those cities and counties that may find their coffers already full from the influx of pandemic-related federal aid and historic sales tax collections. They should also remember the lessons learned during the last housing boom, when millage rates were not rolled-back far enough to avoid Florida’s total property tax bill to increase by 67.2 percent in just four years (FY 2003-04 to FY 2006-07). Many local governments did reduce millage rates, as the total average statewide millage rate for all jurisdictions fell by 9.8 percent over this period. But it was not enough. Many property taxpayers suffered and, when the bubble burst, budgets swollen by this windfall were severely strained.